OVERVIEW

A model is commonly thought of as something that predicts outcomes, however in this case a model is framework for understanding the flow of funds around the world in the financial markets. We use this model to observe and measure the continuous two-way auction process underway in the global financial markets to gain a better understanding of what has happened and how it may continue or change. When there are trends underway we are measuring the strength or weakness of those trends to gain a understanding of the odds of continuation. When there are no trends underway we are observing and measuring the balanced trading ranges and staying alert for a breakout from those ranges which indicates change has taken place and a new directional auction has started.

One of the unique observations from last year's model was that there were not many trends underway at the time. The only trend that was underway was in the two-year treasury and that trend ended up surprising most for its duration and magnitude in 2022. It took until the final month of 2022 for the first sign of change in this trend to appear. It has caused a ripple effect across markets and sets the stage for our review of 2022.

One of the unique observations from last year's model was that there were not many trends underway at the time. The only trend that was underway was in the two-year treasury and that trend ended up surprising most for its duration and magnitude in 2022. It took until the final month of 2022 for the first sign of change in this trend to appear. It has caused a ripple effect across markets and sets the stage for our review of 2022.

Higher inflation was the primary trend in 2022 and as we enter 2023 many are expecting a cyclical downturn in growth and inflation. This has caused the two-year to cease one-time-framing (OTF) higher on the monthly chart signaling an end to the current phase of the upward auction. This could just be a pause before continuing higher, or it could be the beginning of a turn lower in two-year yields. Much will depend on the path of inflation and global central banks' monetary policies and their currencies. There are many opinions about the likelihood of recession in 2023, lower inflation, earnings growth, etc., but we believe that it is best to observe how those opinions are being expressed in the market to be prepared for the different potential outcomes.

The Federal Reserve has raised interest rates at the fastest pace since the early 1980's and that has led to a global trend higher in interest rates across the yield curve and an upside breakout in the dollar index last year. The combination of higher interest rates and a stronger dollar created unprecedented tightness in monetary conditions last year which weighed on risk markets across the board.

The Federal Reserve has raised interest rates at the fastest pace since the early 1980's and that has led to a global trend higher in interest rates across the yield curve and an upside breakout in the dollar index last year. The combination of higher interest rates and a stronger dollar created unprecedented tightness in monetary conditions last year which weighed on risk markets across the board.

However, as we enter 2023 we are seeing a potential upside breakout failure in the dollar index and a downside breakout failure in the Euro. Our focus is on the ability for the dollar and Euro to find acceptance back in the prior multi-year trading ranges which they tried to breakout from in 2022. One of the themes across markets in 2022 was the volatility and thinness of markets. This showed that uncertainty was high and we were not seeing high confidence movement of long-term money in the markets. The fact that the dollar and Euro have not been able to breakout decisively shows that the trend higher in the dollar last year was driven by short-term flows focused on the Federal Reserve's policies. If a new bull market for the dollar was underway we would have seen a more decisive breakout.

As inflation surprised to the upside in 2022 and the Fed and other central banks began to raise interest rates the short bonds and long dollar trade got very popular in the global macro community. Positioning shifted accordingly and until recently has paid off very handsomely. If you look at the lifecycle of a trend through the lens of the Diffusion of Innovations Model you can see that as the trend ages the laggards pile on and accelerate the trend, however they are the weakest investors and are easily shaken out of their positions. This is where we are in the dollar and bonds currently. We saw the market get too long the dollar and too short bonds and those extreme positions are being worked off. What we have seen so far is classic short covering in bonds and long liquidation in the dollar. We do not yet know if that will turn into more sustainable buying of FX and bonds by investors or if the market just needed to come into short-term balance before resuming the trend.

Tight monetary policy and the strong dollar put stocks in a downward trend last year but we have seen a recent short covering rally off the 3500a low which has given the bulls some reprieve into year-end. We know the rally has been a short covering rally because we find a "p-formation" in the weekly bars which shows that the upside advance has slowed and more recently we have seen a downside breakout from the recent trading range. This shows that the buying from the lows was not strong enough to carry through and may have in fact gotten the market too long which led to the recent downside breakout. The focus as we begin the year is on the recent two-week trading range and any breakout from that range will signal the next directional auction. A downside breakout would be a continuation of the primary trend lower whereas an upside breakout could trigger a rally back towards the recent highs. If the market can find upside acceptance above the recent 4100a high it could signal a change in the primary trend lower.

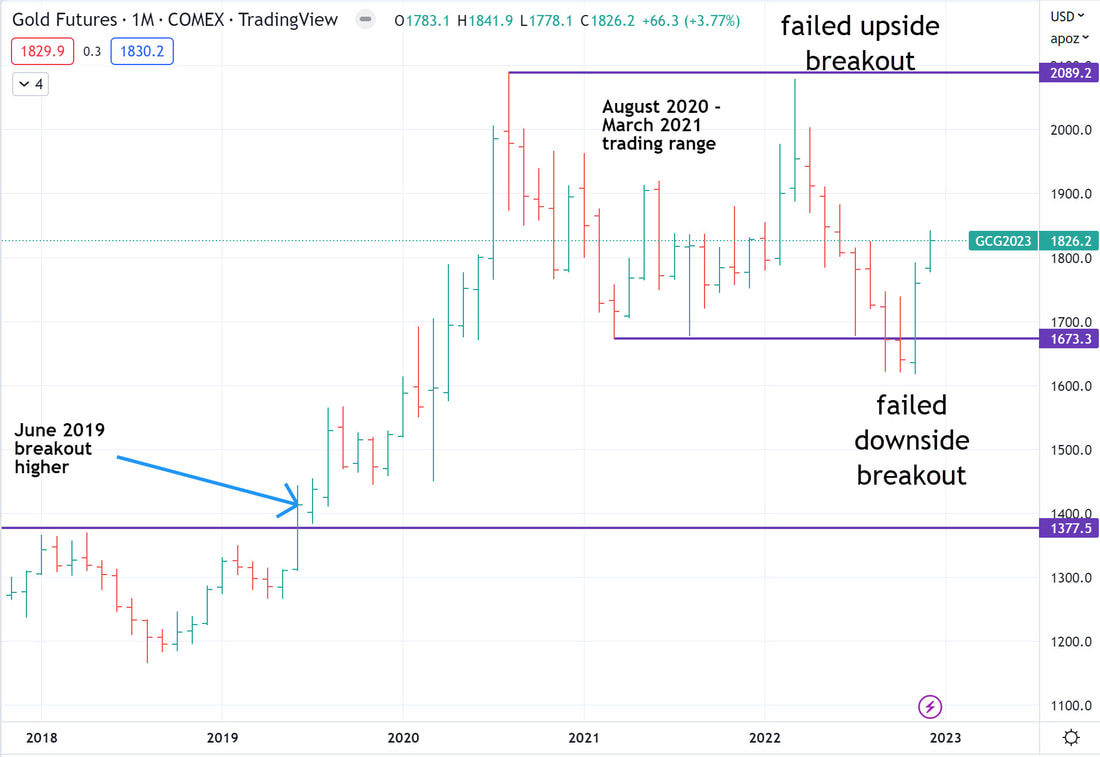

GOLD

The primary trend in gold has been lower since the market almost took out the August 2020 high in March. Unfortunately the panic buying around the Russian invasion of Ukraine did not materialize into anything more and gold suffered under the weight of a higher dollar and higher interest rates. Gold has seen a short covering rally inline with equities, bonds, and FX as the markets have moved to price in a pause in Fed rate hikes but the buying has not been overly strong. In fact, the structure to the rally in gold is very weak and leaves me cautious towards gold. The upside breakout from 2019 has come into a two-year trading range and the market attempted both an upside and downside breakout in 2022 and failed on both tries. A breakout from this two-year trading range that finds acceptance will signal the next directional auction for gold.

BITCOIN

Bitcoin has been in a downward trend since peaking in November 2021. Using Minsky's model of speculation we tend to see the emergence of swindles in the later stages of a speculative mania. I like to use Bitcoin as a proxy for speculation and general risk aversion in the broader marketplace. Benchmarking the speculative mania that we just experienced in the wake of the COVID pandemic with the Minsky model and seeing the emergence of a large fraud in SBF and FTX, we could be seeing signs that we are in the latter stages of the unwind of the post-COVID speculative mania. Be careful not to use any model or any single data point to predict a turn in the cycle, instead use it to understand that we are closer to the end than the beginning in terms of time or price. Auctions have three dimensions: time, price and volume. Remember that close is a relative term and being close to the end can still mean there is significant downside left for price, or that the auction can carry on for several more years. The odds favor that we are closer to the end which means we could see the market languish for a long period of time in a trading range or that we see a sharp drop, followed by a recovery. That being said, it is not an insignificant probability that bitcoin goes the way of Netscape and the dinosaurs.

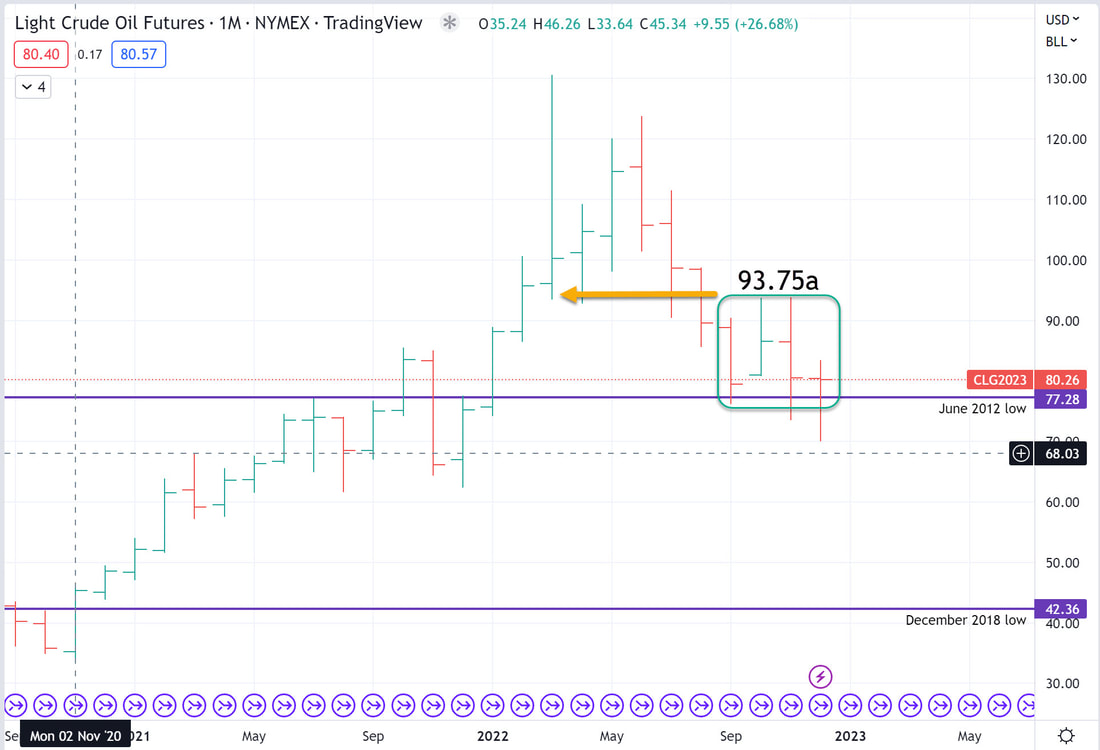

CRUDE OIL

The big surprise last year was the War in Ukraine which pushed energy prices significantly higher across the globe and had a significant impact on inflation. Oil prices rocketed through $120/bbl and many are expecting $200/bbl oil in the future due to supply constraints from years of underinvestment due to the ESG movement. Once again the market got ahead of itself early in the year and we saw oil prices fall back through $100 later in the year as concerns about global growth began to grow. Narrative follows price and nowhere was this seen better than in the energy markets in 2022.

The trend has turned lower in crude oil but the market has come into a rough four-month trading range with support near the $76-77 level. The COVID lockdowns in China cut Chinese demand for crude and has added to the pressure on the market after the speculative peak earlier in the year. The market recently looked below support and has come back into the monthly trading range which could set the stage for an upside breakout above the $93-$94 resistance level later on. The trend lower is either slowing down or consolidating and how the market handles this four-month trading range will determine the next directional move for crude.

Crude will be an important barometer in 2023 as China re-opens and the world is focused the outlook for growth and inflation. 2022 was one-dimensional in its focus on inflation and 2023 will likely see a two-dimensional focus on the trade-off between growth and inflation. Higher crude prices would signal improved growth prospects, however they would also put upwards pressure on inflation.

Crude will be an important barometer in 2023 as China re-opens and the world is focused the outlook for growth and inflation. 2022 was one-dimensional in its focus on inflation and 2023 will likely see a two-dimensional focus on the trade-off between growth and inflation. Higher crude prices would signal improved growth prospects, however they would also put upwards pressure on inflation.

YEN

The BOJ resisted tightening their monetary policies despite the Fed's aggressive actions until late in 2022. The BOJ intervened multiple times in their FX markets and also raised the cap on interests rates that is part of their YCC operations. The divergence in monetary policy put extreme pressure on the Yen and it broke out of its six-year trading range. Now with the Fed signaling a slow pace of rate increases and the BOJ starting to shift their policies the Yen has come back down to 130a support. The short Yen trade was another popular trade last year and positioning got very short as shorter-term traders were gunning for the 150a which they finally got in October and since then the market has been straight down. If the Yen finds acceptance back below the 2015 high and in the prior trading range we would have an upside breakout failure in the Yen to go along with the Euro and put further pressure on the dollar which could be supportive for risk markets.

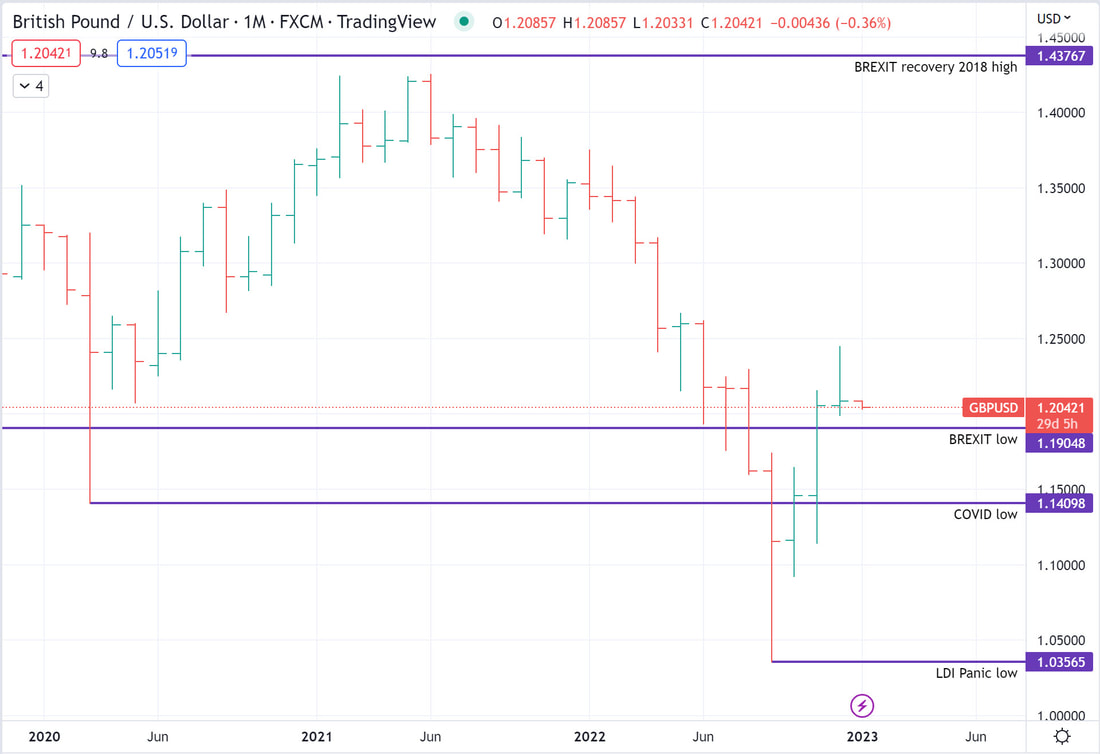

BRITISH POUND

Leading the pack for the short dollar trade is the Pound. It is said that the Fed often tightens until something breaks and in this cycle it was the the UK that broke. After taking out the COVID lows amidst the liability-driven-investing panic and seeing the BOE restart bond purchases to support the Gilts market, the Pound has found an excess low and has started to trend higher. The downside breakout attempt failed, left an excess low and has found acceptance back in the prior Brexit trading range. The pound is the first of the major crosses to find acceptance back in its prior trading range. Failure to maintain acceptance would be notable and could signal continued strength in the dollar. The Pound closed near the December lows and an early cessation of OTF higher on the monthly chart would be the first sign of caution for the Pound.

Conclusion

2022 saw unprecedented Fed tightening which put pressure on risk markets, broke the speculative bubble from 2020-2021, and caused a panic in the UK Gilts market. The primary trend is lower for risk markets but as we enter 2023 we are seeing early signs of change from the treasury market and the FX markets. The UK market appears to have put in an excess low and began a new upward trend, but the rallies we are seeing elsewhere in treasuries, gold, the Euro, and the Yen so far look like short covering rallies. Trend reversals in a bear market typically start with short covering rallies that attract further buying interest as the economic fundamentals change and higher prices attract more buyers. It is too early to know if economic fundamentals are changing and if higher prices will attract further buying interest. The emergence of massive fraud in the crypto market is a sign that we are nearing the end of the unwinding of that speculative bubble, but how and when that plays out remains highly uncertain. Focus remains squarely on monetary policy and inflation, but growth and the growth-inflation trade-off will increasingly come into play during 2023. It is normal to see a cyclical downturn in inflation which we began to see in late 2022, but experience from the 1970s shows that inflation typically comes in waves so the odds of another wave of higher inflation cannot be ruled out.

Without clear resolution on the economic and monetary policy fronts it will be hard for larger investors to make any decisive shifts in their portfolios. This increases the odds that we will continue to see thin markets and volatile trading conditions. An expected shift in monetary policies could lure some off the sidelines but we will have to stay tuned to the risk of a second round of inflationary pressures later in the year or next year.

Without clear resolution on the economic and monetary policy fronts it will be hard for larger investors to make any decisive shifts in their portfolios. This increases the odds that we will continue to see thin markets and volatile trading conditions. An expected shift in monetary policies could lure some off the sidelines but we will have to stay tuned to the risk of a second round of inflationary pressures later in the year or next year.